The PolyAsset Portfolio

Strategic Architecture for Capturing Crypto’s Next Order of Magnitude

Lucrum Verus Capital’s Polymorphic Rails thesis rests on a simple conviction: the economic surface area of crypto can scale by an order of magnitude over the next decade. If the last era of crypto was about proving that decentralized systems could exist and flourish, the next era is about those systems becoming default plumbing for a meaningful slice of global finance and commerce.

The critical question for a convicted investor is not whether crypto can grow. The question is: if the system grows 10x, which claims capture that value and when?

Our answer is a portfolio architecture designed to reduce value-capture model error.

We call it the PolyAsset Portfolio.

One ecosystem, multiple wrappers

Crypto is often described as an asset class. In practice, it is better understood as an ecosystem where the same underlying activity can be expressed through different legal and financial wrappers.

A network or business might begin life as a venture-backed startup: a Delaware C-corp raising priced rounds. As it matures, it might:

remain private for years, compounding quietly,

be acquired by a strategic buyer,

go public through a conventional IPO,

launch a token that becomes the primary economic interface to a network,

or transition across multiple formats over its lifecycle.

Meanwhile, the infrastructure that supports it—exchanges, brokers, custody, market makers, stablecoin issuers, payments rails, data providers—may exist as a mix of open networks, private companies, and public enterprises.

The result is a market where the same secular trend can produce investable opportunities across multiple claim types at once. A strategy that touches only one wrapper can be directionally right and still structurally underexposed or exposed to the wrong claim on the right trend.

Why not just pick one? Because the best opportunity is path-dependent

If you knew in advance exactly where value would accrue (protocol tokens versus application-layer businesses versus regulated incumbents) then concentration could be optimal.

In reality, value capture in crypto is path-dependent and contested; meaning we can’t precisely predict tomorrow’s outcomes based on today’s variables. What happens tomorrow effects what happens next week, and different forces are competing fiercely to determine that path of progression.

Some ideas reward liquid network claims because adoption expresses itself first in coordination, liquidity, and reflexive network effects.

Some ideas reward private equity because durable businesses compound quietly long before public markets re-rate them.

Some ideas reward public operators because regulation and institutionalization push profit pools toward scaled, compliant intermediaries.

We treat each wrapper less as a separate “bucket,” and more as a competing claim on the same adoption curve. The PolyAsset Portfolio is designed to diversify across those claims. Ideally, our outcomes depend less on being perfectly right about where value accrues and more on being right about what is happening in the ecosystem.

A single-wrapper strategy is a concentrated bet on one value-capture regime. The PolyAsset Portfolio is a bet on the underlying adoption curve while reducing the probability that we are right about the world but wrong about the wrapper.

This is the specific error we are trying to avoid: value-capture model error.

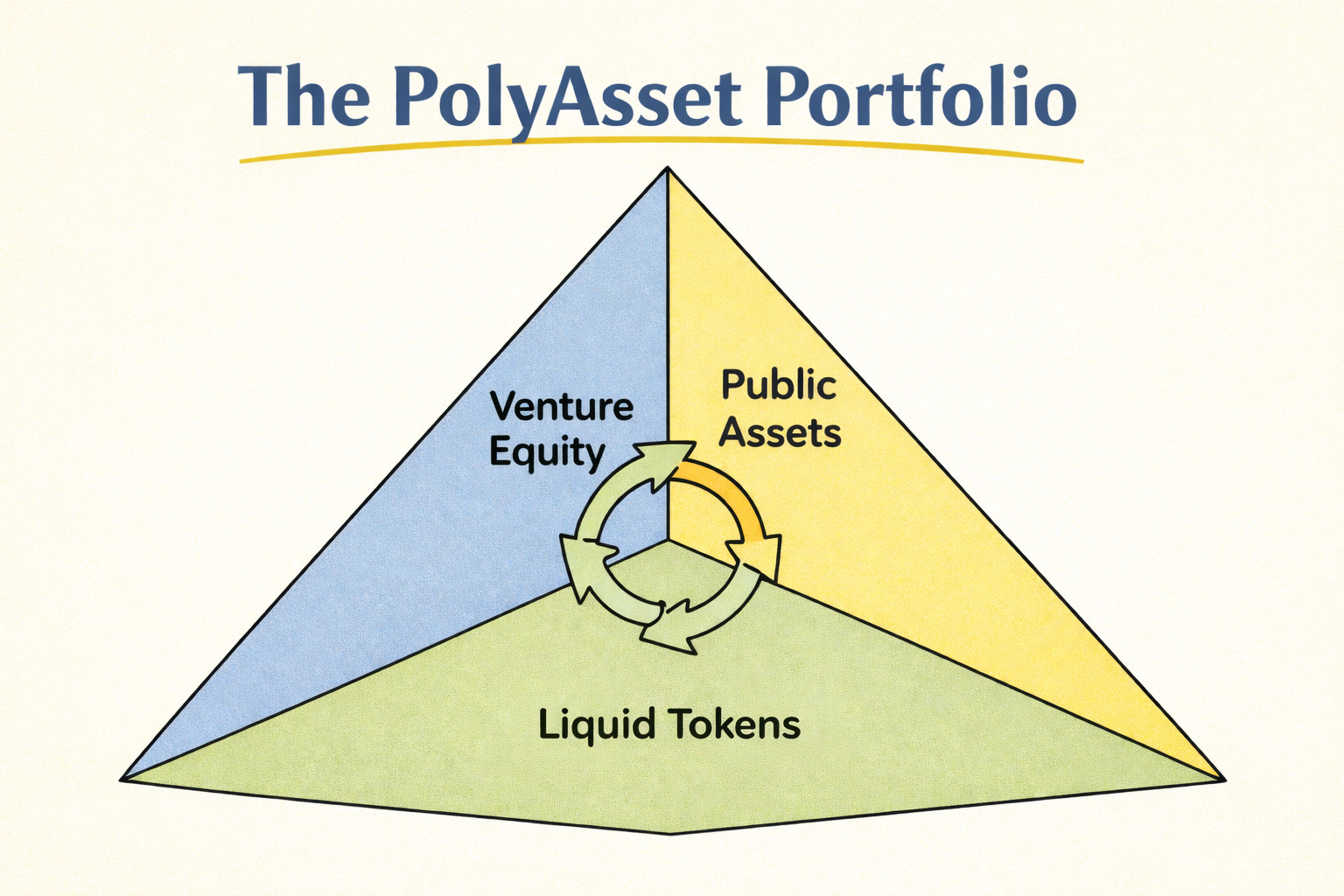

The PolyAsset Portfolio

The PolyAsset Portfolio is our framework: one unified thesis expressed across three complementary asset classes.

Venture equity in high-growth startups building distribution, applications, and key infrastructure.

Liquid digital assets (tokens) that sit closest to onchain activity and network coordination.

Public equities and public-market vehicles that capture scale, compliance advantages, and durable profit pools as crypto integrates with regulated finance.

Accessing multiple asset types enables a portfolio architecture built to accomplish three interlocking goals:

1) Preserve survivability and optionality across cycles

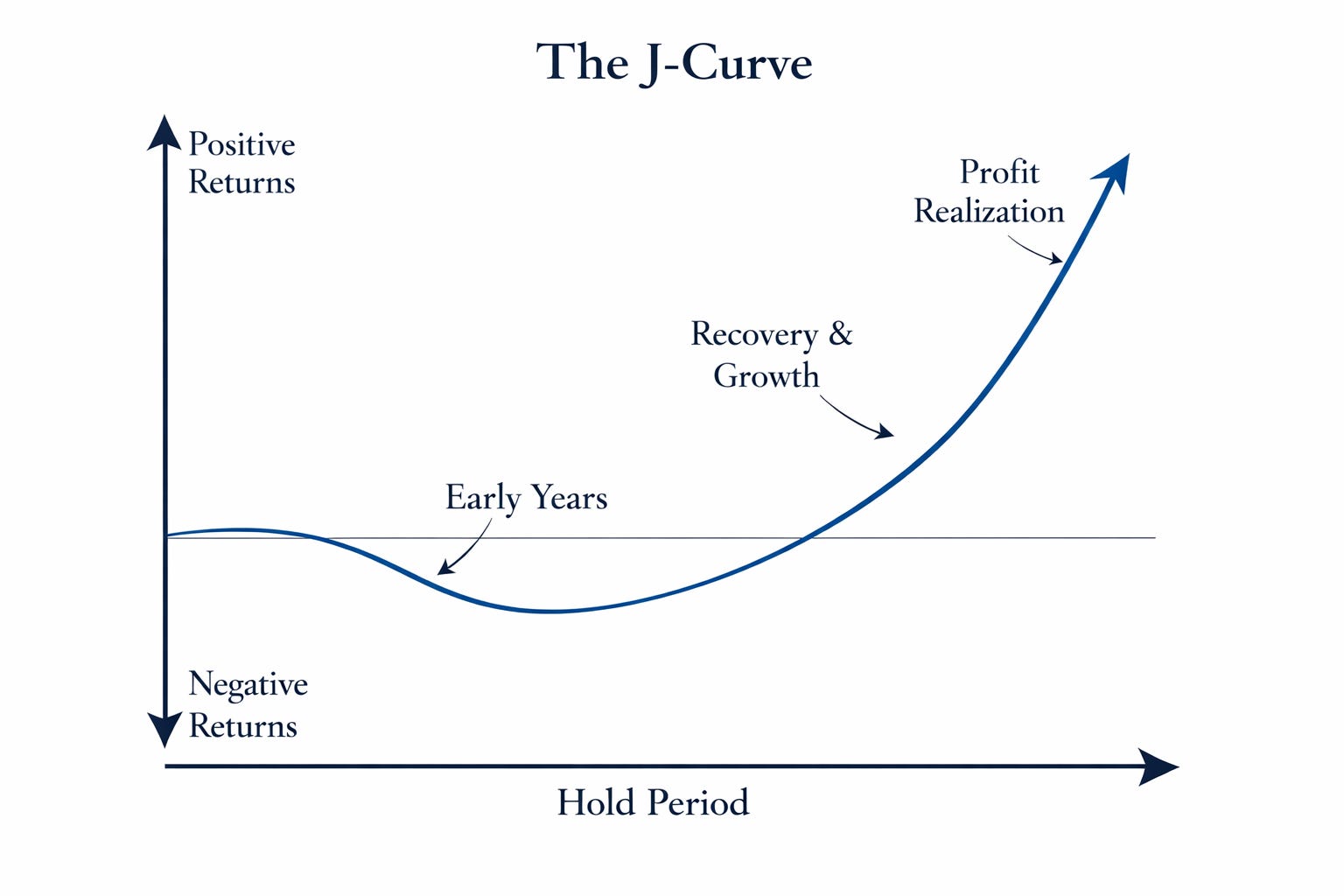

Private funds, particularly in venture, tend to follow a J shaped return curve: capital is deployed early, fees accrue, and real value creation takes time to show up in marks and liquidity. That is not a flaw; it is the time geometry of private markets.

The purpose of a liquid sleeve is not to promise smooth returns. It is to preserve optionality.

Liquid markets allow us to size exposure, manage risk when regimes change, and re-underwrite opportunities during dislocations: capabilities that do not exist once private capital is locked. Used prudently, these tools can reduce the probability of forced errors in downturns and improve our ability to stay opportunistic across cycles.

To be explicit: liquidity does not guarantee positive returns, and crypto drawdowns can be severe. The point is not that liquid markets are “safer.” The point is that they allow for position sizing, hedging, and exposure management that are unavailable in private markets; tools that can be used to avoid avoidable mistakes when the environment changes.

2) Keep the learning loop tight across the full lifecycle of adoption

Crypto is unusual in that the market is both a capital market and a product environment. Network usage, liquidity migration, developer adoption, and regulatory signals often show up first as measurable system behavior (fees, throughput, spreads, and stablecoin flows) before they show up as consensus narratives,

Being active across classes keeps us close to the entire lifecycle:

Liquid markets can reveal where coordination is concentrating: liquidity hubs, settlement preferences, stablecoin routing, and changing market structure.

Private-market diligence can reveal where talent, execution, and distribution are compounding before the market can price them.

Public markets can reveal where regulation is pushing profit pools, which business models can scale inside the rules, and when institutional adoption becomes economically durable.

This learning loop only matters if it is disciplined. Our intent is to translate signals into a consistent investment process—using observable indicators to refine our view of what the rails are becoming, and then expressing that view through the most attractive claim type available.

3) Follow quality across formats

The strongest opportunities in crypto do not reliably appear in one wrapper. In practice, some simple heuristics can be tracked:

Prefer tokens when:

the network’s economic design creates a credible path to durable value accrual (not just attention accrual),

the moat is coordination, liquidity, or composability,

liquidity is an advantage

Prefer venture equity when:

the moat is distribution, product execution, enterprise workflow, or regulatory licensing,

the business captures value through revenue and control rather than protocol-level economics,

the compounding happens before public markets can efficiently price it.

Prefer public markets when:

regulation and institutionalization consolidate profit pools toward scaled, compliant operators,

governance clarity and operating leverage matter more than protocol design,

the public market is mispricing the pace or inevitability of adoption.

These rules keep the sleeves complementary rather than redundant, and keep us honest about what, exactly, we are underwriting.

Hybrid portfolios struggle in predictable ways and must be intentionally controlled for

Multi-claim strategies are obviously desirable, but can be devilishly hard to operate. Several failure modes are well-known and must be controlled for:

Liquidity mismatch: illiquid private holdings paired with liquid liabilities can limit capacity to execute on certain opportunities when desired.

Correlation spikes: in periods of stress, diverse assets within the same ecosystem (crypto) can move together.

Style drift: a liquid sleeve on top of a promising venture practice can slowly become undisciplined trading.

Marking asymmetry: liquid marks move fast; private marks move slow, thus obscuring true performance.

A PolyAsset strategy is not a failsafe bulwark against volatility. It requires disciplined execution governed by sleeve-level mandates, risk budgeting, and reporting designed to prevent hidden fragility.

Each sleeve must earn its place with a distinct role; long-duration convexity (venture), adoption and coordination exposure with fast feedback (tokens), and institutional profit-pool capture (public).

What PolyAsset thinking might look like in practice

The same theme can often be expressed through multiple claims. Our job is to choose the claim with the best risk-adjusted path to durable capture.

Payments and stablecoin distribution.

The token expression can be attractive when network effects and routing are the moat. The equity expression can be superior when distribution, partnerships, and compliance determine outcomes. Public operators can become compelling as scale and licensing consolidate margins.

Onchain market structure.

Tokens can reflect coordination around liquidity venues and settlement hubs. Private companies may capture the tooling and workflow layer. Public markets may capture the regulated interface as institutions adopt.

Tokenization and institutional rails.

Early on, infrastructure builders can compound privately. As the market matures, profit pools can shift toward scaled, regulated intermediaries with governance clarity.

The point is not to own every wrapper. The point is to own the best claim on a theme as the ecosystem evolves.

A broader backdrop: the boundary between public and private is dissolving

Even beyond crypto, the global financial system is experiencing a convergence of asset classes and market structures.

Retail investors increasingly want exposure to high-performing private companies long before IPO. Sophisticated hedge funds routinely run cross-asset playbooks spanning everything from tech equities to commodities to crypto. Regulators are being pushed (by market innovation and political reality) to modernize frameworks around custody, market structure, and tokenization. And advances in software and AI are making complex strategies operationally feasible for smaller, more focused teams.

Crypto is not causing this convergence by itself, but it is accelerating it. Crypto rails make assets more programmable, settlement more continuous, and financial products easier to compose.

The PolyAsset Portfolio embraces this reality rather than fighting it.

Durable Capture in an Evolving System

PolyAsset Portfolio thinking is built for the world where crypto stops being a category and becomes infrastructure. In that world, the biggest mistake is not being early: it’s being right about adoption and wrong about where value accrues. Our strategy is designed to stay pointed at the rails as they evolve, to own the strongest claim on durable growth as wrappers shifts, and to compound through cycles with discipline rather than improvisation.